Ethereum governance experiments have produced an incredible variety of coordination mechanisms: project/token DAOs, Moloch DAOs, Nouns DAOs, retroactive public goods funding, quadratic funding, and more. Yet many of these models share the same structural weaknesses (speculation, finite runways, and governance fatigue) often resulting in reflexive collapse.

What if we designed an institution optimized not for token price or short-term capital deployment, but for permanence?

This post introduces the Perpetual Endowment Network (PEN), a conceptual model for a permissionless, member-governed on-chain endowment designed to preserve capital indefinitely while allocating only its yield through decentralized governance.

The goal of this article is not to present PEN as a finished system. Instead, it is meant to introduce the core mechanisms and invite discussion from the Ethereum community.

The Core Idea

A PEN is a permissionless institution where members collectively govern an endowment whose principal is never spent. Instead, a PEN only distributes the yield generated by that principal.

Members participate by purchasing seats, which grant voting rights. Seats are non-transferable and represent non-delegatable voting power in periodic funding decisions.

The system is designed around a few key constraints:

- Capital preservation: principal remains intact indefinitely

- Periodic governance: votes only occur at predictable intervals

- Slate voting: members vote on funding slates rather than individual proposals

- Non-speculative participation: seats do not receive distributions and cannot be traded

The PEN model attempts to create a permanent on-chain funding institution governed by members rather than token markets.

Soulbound Seats

Membership in a PEN is represented by seats, which have several unusual properties compared with typical DAO governance tokens:

- Fixed maximum supply

- Seats can be purchased for oneself or others

- Seats are non-transferable (soulbound)

- Seats can be voluntarily resigned with a partial refund

- The PEN can reclaim inactive seats

- One seat = one vote

- No delegation of voting power

Members cannot sell or transfer seats, nor delegate voting power. Governance participation is tied directly to membership in the PEN itself and cannot be accumulated through secondary markets for seats or votes.

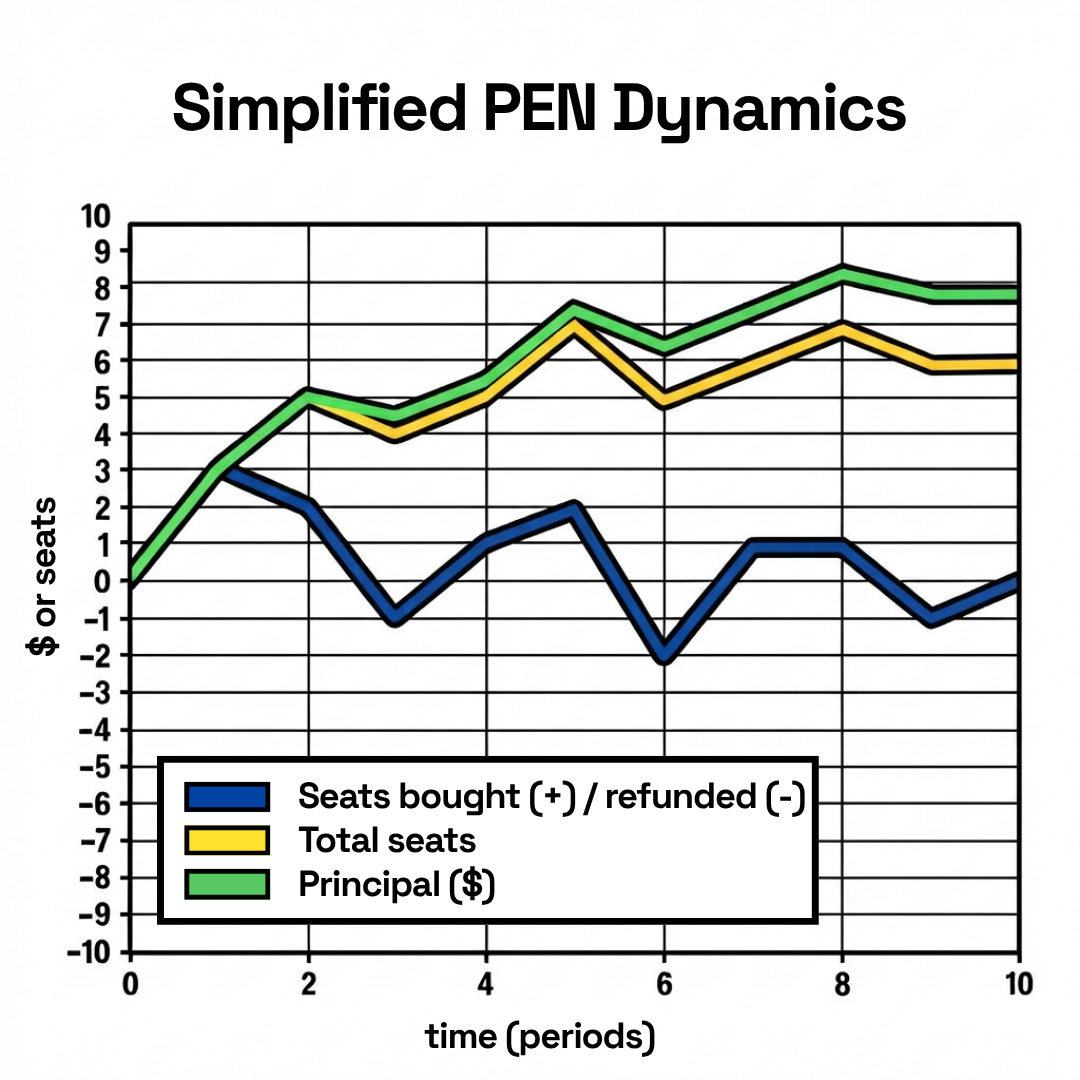

Seat Purchases, Resignations & Reclamations

Anyone can permissionlessly purchase seats, which are sold via floating bonding tranches contract — i.e. seat prices increase (or decrease) as more seats are purchased (or resigned/reclaimed). The floating bonding tranches ensure that early members receive a lower seat price than later members. This setup helps bootstrap the network. It is also recognizes that early members take more risk and responsibility than later members.

Members can resign their seats by burning the seat and claiming a fixed price refund (which is always significantly lower than the lowest seat purchase price). Resignations allow for members to rage-quit if their values no longer align with those of the PEN. However, resignation is always painful for the departing member. The PEN can also reclaim inactive seats if a member does not vote for 12 months.

The interplay between these purchases, resignations and reclamations gives the PEN a wonderful anti-fragile property. Seat refunds and reclamations may cause the seat price to move to a lower tranche and always leaves the PEN more well capitalized per member. This creates two structural feedback loops that dampen negative dynamics and prevent reflexive collapse. Departures benefit members who stay, preventing further departures. Departures make new seat purchases more attractive for both new and existing members, spurring new growth.

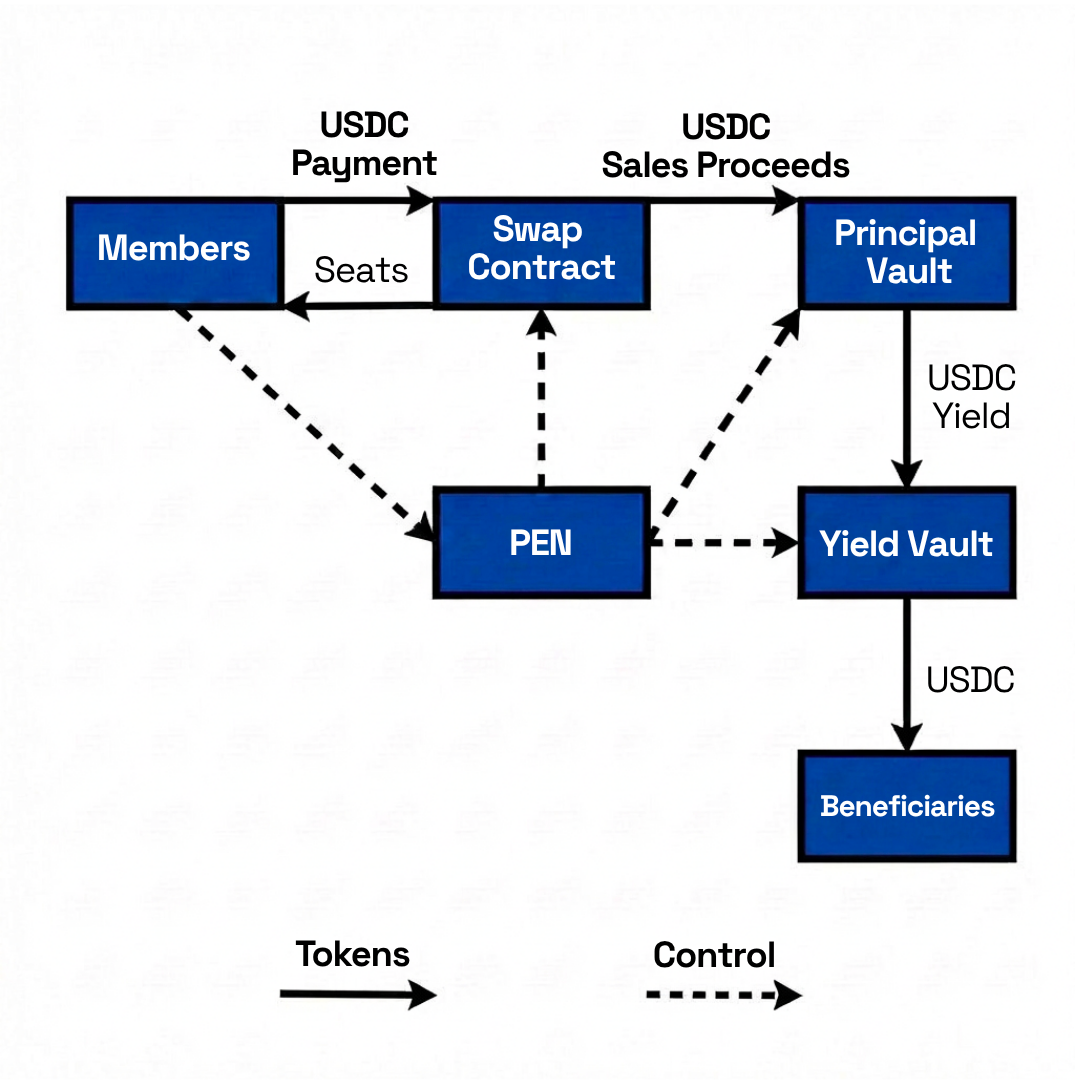

Two Vault Treasury

The treasury design separates capital into two distinct vaults:

The Principal Vault stores the core endowment, which is allocated into yield-generating strategies, but never spent.

The Yield Vault receives yield from the Principal Vault, which is distributed or reinvested via a quarterly vote.

This separation is crucial: it prevents the classic DAO failure mode where treasuries are slowly drained through governance decisions.

One Slate Vote Per Quarter

Governance in a PEN intentionally avoids the constant proposal churn common in many DAOs. Instead, a PEN schedules one funding decision once per quarter.

Anyone can submit a funding slate, which represents a complete allocation of that quarter’s yield. Members then vote using ranked-choice voting across:

- the default option of reinvesting the yield back into the Principal Vault

- competing funding slates, which include funding for value-aligned projects and PEN operations

The winning slate determines how the yield is distributed.

This structure simplifies and compresses governance activity into predictable intervals and reduces voter fatigue while still allowing open participation.

Conviction & Status, Not Speculation

PENs reshape incentives around governance participation — attracting people and organizations motivated by values and the desire to accrue social capital, not financial gain.

Members purchase seats to signal alignment, steward capital toward shared goals, gain influence over funding decisions, and build a reputation within the PEN and broader ecosystem.

Members do not receive financial distributions from the PEN, nor can they sell their seats for a profit. A PEN is similar to a TradFi member-governed foundation. It is clearly not a financial investment vehicle.

Health Indicators

The growth, maturity and health of a PEN can be evaluated using the following indicators:

- Principal (AUM) — the value of assets under management

- Annual Yield Rate (rAUM) — how much annual funding the principal generates

- Number of occupied seats (N)

- Price according to bonding tranches (P)

- Principal per seat (AUM/N) — how much principal a seat governs

- Annual Yield per seat (rAUM/N) — how much annual yield a seat governs

- Governance price ratio (GPR = (A/N)/P) — how much principal a seat governs relative to its price

- Yield price ratio (YPR = (rA/N)/P) — how much annual yield a seat governs relative to its price

In particular, the GPR and YPR help signal whether entering the network is attractive to new members.

As mentioned above, seat refunds and reclaims increase these ratios, which means that attrition makes seats more attractive to new and existing members.

Operational Simplicity

The PEN model seeks to minimize permanent organizational structures, entrenched managers and rent-seeking actors.

Operational work (such as maintaining interfaces, coordinating rounds, or facilitating governance) can be performed permissionlessly by anyone. Anyone can observe PEN actions or contribute to its growth, but no one can speak or act on behalf of the PEN. This operational work is then funded retroactively through funding slates, rather than through fixed budgets or core team allocations. This arrangement keeps the institution lightweight and meritocratic while still allowing important operational work to be compensated.

System Components

A minimal implementation of PEN could consist of:

- Seat token contract: tracks governance seats

- Bonding tranche contract: seat pricing, sales, and refunds

- Principal and Yield vaults: handle capital and yield

- Onchain voting system: manages voting for onchain proposals and transaction execution (e.g. deploying/closing a Principal Vault, distributing yield, closing the PEN)

- Offchain voting system: manages voting for offchain proposals (e.g. slate votes)

- Community forum: discussion and coordination layer

- Bonding tranche contract UI: user-friendly seat sales and refunds

- Dashboard: transparency around AUM, seat distribution, and funding history

The architecture intentionally uses configurable parameters and modular components so different implementations can experiment with variations.

On The Shoulders of Bull-Headed Idols

The PEN model is inspired by earlier Ethereum coordination and funding models. It seeks to build on their excellent work, and also explore fundamentally different mechanisms.

Alignment with Ethereum

Ethereum continues to search for sustainable funding models for its own public goods, and it strives “to be civilization-scale infrastructure that securely underpins the internet and global economy, surpassing the safety and trustworthiness of the world’s legacy systems”.

A PEN offers a new onchain implementation of a traditional model: permanent capital with governance-directed yield. If widely implemented, PENs could fund ecosystems, research, infrastructure, and cultural initiatives for decades, even centuries. And in doing so, they could bring millions of value-driven people into the Ethereum ecosystem.

Open Invitation

The Perpetual Endowment Network (PEN) proposes a new experiment in decentralized onchain organizations: a permanent, member-governed funding institution built around capital preservation and periodic collective judgment.

If the idea resonates (or if you see flaws) we’d love to hear your thoughts.

Add your feedback here: https://shutternetwork.discourse.group/t/feedback-on-the-perpetual-endowment-network-pen/842

What would you change? What assumptions should be challenged? And what kinds of ecosystems might benefit from a model like this?

The discussion is open.